By Cory McPherson

May 29, 2026

With the market indexes continuing higher in May, the semiconductor industry has been by far the leader of the charge. It has not been a broad-based rally with many different industries participating that would typically lead to a healthier environment. But the move by semiconductor stocks has been so extreme it has led the S&P and Nasdaq indexes to look parabolic in their move higher since the end of March. In this newsletter I’ll compare this move by semiconductors to a past historic move and what that may pertain for what’s to come.

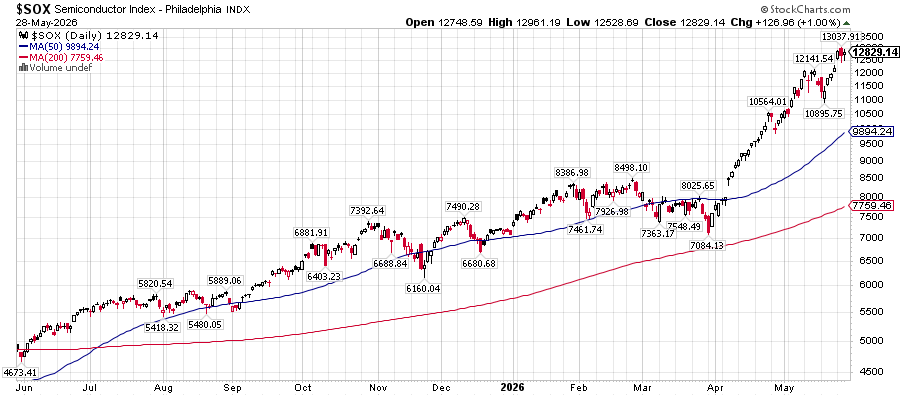

The benchmark for semiconductors can be tracked through the PHLX semiconductor index, known as SOX. That index has soared over 79% year to date, its best performance for the first 100 trading days of a year. It consists of 30 different stocks, and each are up more than 10% so far this year, which is more than the S&P 500 itself has returned. You can see from the chart below the rapid increase in the index since the end of March, a return of over 81%. It is now well extended above its 200-day moving average and would take a drop of over 39% just to get back to that long-term average. Yet that would still be above where it was at the end of March.

The industry has been buoyed by the artificial intelligence buildout and demand for computer chips. And it hasn’t been just the biggest chip makers making the biggest moves. The biggest by market cap, Nvidia, has actually underperformed its industry peers this year. One of the biggest gainers this year, Intel, had been the industry’s biggest laggard for several years. Market leadership has been concentrated to this industry, similar to what we’ve seen for much of the last 10 years. Although previously it was the “Magnificent 7” big tech stocks that led the way, this is more defined to one industry. In fact, a few of the big tech stocks have not participated much in this recent rally.

With this extreme move in such a short amount of time, it has driven comparisons to the dot-com days of the late 1990’s and ensuing bursting of the tech bubble. Like most things, there are similarities but also differences to that time. The below chart actually shows this same semiconductor index and how it performed from 1999 to 2000, showing the end of the tech bubble. From March 1999 to March of 2000, the index was up about 300%. By the end of 2000 though, it had fallen almost 60% from its peak. By the end of 2002, the bottom for the stock market, the index had more than erased all gains from 1999 to March of 2000 as the unwinding was complete.

The recent move in semiconductors could very well have higher to go and become even more extreme. No one can predict when it will top. The biggest move during 1999-2000 happened at the end of the cycle, as price more than doubled in the last 3 months before the peak. What history tells us with any investment is when something moves in a straight up fashion, they don’t keep going straight up. And the more extreme something gets the bigger the eventual unwind. A parabola pattern eventually presents itself. The chart from semiconductors from 1998-2002 shows that very pattern, as seen below.

A difference from the current period to the tech bubble days is in valuations. While price-to-earnings ratios today for semiconductor stocks are very rich at roughly 80x, it is below some of the tech and telecom names from the 1999-2000 period that had price-to-earnings ratios of 500x or more. Today’s companies have also been reporting very healthy profit growth and forward guidance on revenues. The rapid increase in forward guidance from some of the semiconductor stocks has gone hand-in-hand with their stock price rocketing higher. Many of the popular names during the tech bubble never actually had any earnings. The question today for semiconductor companies on a fundamental basis is how long can the hyperscalers continue to spend at their current pace without a return on investment. The big spenders on AI consist of Amazon, Microsoft, Google, and Meta, and they are projecting to spend over $700 billion on AI capital expenditures this year. Their focus currently seems to be winning the race at any cost regardless of return. That won’t be able to continue forever.

History is littered with examples of investments moving in a straight up fashion with a sense of euphoria from investors. The claim is always, “this time is different.” Yet, the ending is always the same. Eventually, we’ll see that play out with semiconductors again. How it unwinds and when is unknown.

Cory McPherson is a financial planner and advisor, and President and CEO for ProActive Capital Management, Inc. He is a graduate of Kansas State University with a Bachelor of Science in Business Finance. Cory received his Retirement Income Certified Professional (RICP®) designation from The American College of Financial Services in 2017.

DISCLOSURE

ProActive Capital Management, Inc. (PCM”) is registered with the Securities and Exchange Commission. Such registration does not imply a certain level of skill or training.

The information or position herein may change from time to time without notice, and PCM has no obligation to update this material. The information herein has been provided for illustrative and informational purposes only and is not intended to serve as investment advice or as a recommendation for the purchase or sale of any security. The information herein is not specific to any individual's personal circumstances.

PCM does not provide tax or legal advice. To the extent that any material herein concerns tax or legal matters, such information is not intended to be solely relied upon nor used for the purpose of making tax and/or legal decisions without first seeking independent advice from a tax and/or legal professional.

All investments involve risk, including loss of principal invested. Past performance does not guarantee future performance. This commentary is prepared only for clients whose accounts are managed by our tactical management team at PCM. No strategy can guarantee a profit.

All investment strategies involve risk, including the risk of principal loss.

This commentary is designed to enhance our lines of communication and to provide you with timely, interesting, and thought-provoking information. You are invited and encouraged to respond with any questions or concerns you may have about your investments or just to keep us informed if your goals and objectives change.