By Cory McPherson

March 27, 2026

While my expectation going into the year was for a more volatile and choppy market, I did not expect the type of noise that we’ve gotten around the market with what’s going in the world. With bombs being dropped and missiles shot all over the Middle East, Americans here at home are fearful of what this conflict may turn into. This fear has obviously led to lower stock prices and much higher oil prices this month. Despite that, though, the selling that has occurred in the stock market so far has been controlled. We have not seen any type of “crash”-like behavior yet, which is what we saw around this time last year. In this newsletter, I’ll look at past world conflicts and how the market behaved, what is happening in private credit and why it is a concern, and other issues that may influence the market in the months ahead.

Looking at the S&P 500 chart below, the sideways consolidation we had been in has broken to the downside this month. We now sit below the 200-day moving average (red line) for the first time since last April/May. It is also sitting below the lows made in November last year. So far, though, this is just an ordinary pullback, sitting about 8% now below its all-time high. In order to stave off any trapdoor lower, it needs to start showing some strength soon and at the least get back up into the range that it was in to start the year. In my last newsletter, I showed how the large technology stocks that are the leaders of the market have been struggling for the last few months even while the market remained near its highs. Those stocks have continued to struggle and have not found any sustained rally and have begun to drag other parts of the market lower. Obviously, the fear of what is happening in the world has aided in that.

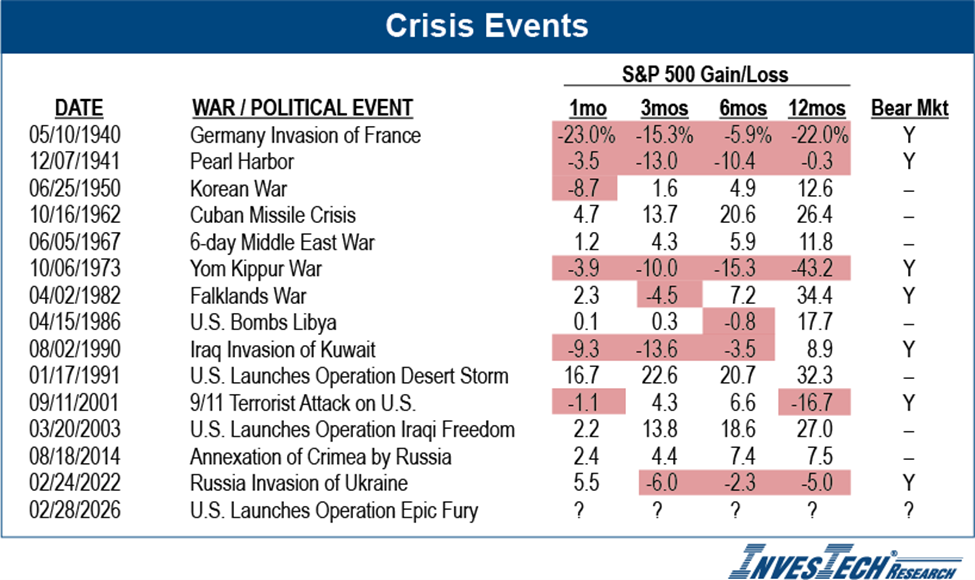

While it is easy to believe that any international crisis or war will lead the stock market lower over time, history doesn’t bear that out. The graphic below from InvesTech Research shows past conflicts going back to World War II and what the S&P returned the following month, 3 months, 6 months, and 12 months. The only thing that’s clear is that there is no clear pattern in how the S&P 500 will react over the next several months, even if this conflict drags on.

In most of these cases, the market continued the trend that it was already in before the conflict began. If you look at the last two similar events for our country, the 2003 operation in Iraq, and the 1991 Desert Storm operation, the market reacted positively over the next several months. But what you must remember is where the market was before those events. In 2003 we were coming out of the unwinding of the tech bubble that popped in 2000. The market had recently bottomed out and began its next uptrend until the great recession in late 2007. In 1991 we were beginning to come out of a recession and the market bottomed out in late 1990 and had begun its next trend higher. The market going into this current conflict did not have the same characteristics. In the short term we were trendless going sideways, and in a long-term uptrend going back now almost 17 years, not the beginning of a new uptrend. What this shows is, historically, wars or crisis events by themselves won’t make or break the market in the long run.

What has a better chance of breaking the market are economic and credit issues here at home. Issues in private credit have begun to create some headlines recently, but most everyday Americans don’t know what private credit is or what problems it is having. Private credit is money being loaned out by non-bank financial institutions, many by private equity and alternative asset managers to small and mid-sized businesses. These are businesses that for different reasons cannot borrow in corporate bond markets or from traditional bank loans. So, they look for an alternative from non-bank financial institutions for financing. Some call it “shadow banking”.

Since these are non-bank institutions lending money, it differs from how traditional banks lend money. Banks take short-term deposits and create long-term loans. These non-bank institutions like private equity firms raise long-term capital from investors, typically high net worth individuals and institutional investors like pension funds and insurance companies. They can then either purchase equity stakes in businesses or make loans to businesses, creating private credit. Private credit has grown rapidly since 2008, as the aftermath of the banking and financial crisis led to new regulations and tighter lending standards for traditional banks. Many businesses then had to turn to alternatives for financing. In just the last five years it has gone from $500 billion to $1.3 trillion. Why would someone invest in private credit? Much of its growth can be attributed to higher yields offered compared to traditional fixed income with historically lower volatility. That is beginning to change, though.

Access to participate in private credit funds historically has been limited to those high-net-worth individuals and institutional investors. Over the last few years, though, funds have lowered thresholds and opened up to “retail” customers to invest in private credit. What is beginning to make headlines is that these funds are limiting or completely restricting investor withdrawals from their funds. Typically, when you invest in private credit, access to your capital can be restricted to only certain periods to prevent any type of “run on the bank” scenario and you receive interest/dividends back over time. Here recently, many private credit funds are limiting what investors can take out during liquidation periods or not allowing any money out at all.

Why are investors wanting their money out? There has been a spike in defaults occurring and a markdown in credit quality in many of these funds. Historically defaults in private credit lending are 2-2.5%, but Morgan Stanely recently warned default rates could surge to 8%. Recent private credit fund managers that have curbed investor withdrawals include Ares Management, Apollo Global Management, Blue Owl Capital, and Cliffwater. Is this a risk similar to the mortgage lending that led to the financial crisis and great recession? It’s too early to tell, but something to certainly watch. How regular banks, especially the big banks of this country, are intertwined with these private credit funds will be important. Private credit problems can definitely spread and create a domino effect into other parts of the economy as it relates to liquidity and access to funding. Right now the talking heads on Wall Street and executives of these private credit funds believe any problems in private credit will be contained and won’t present a systemic risk similar to 2008. But remember, similar things were said in 2006-2007 in the lead up to the financial crisis of that period, and most of these folks will not be warning you of their problems.

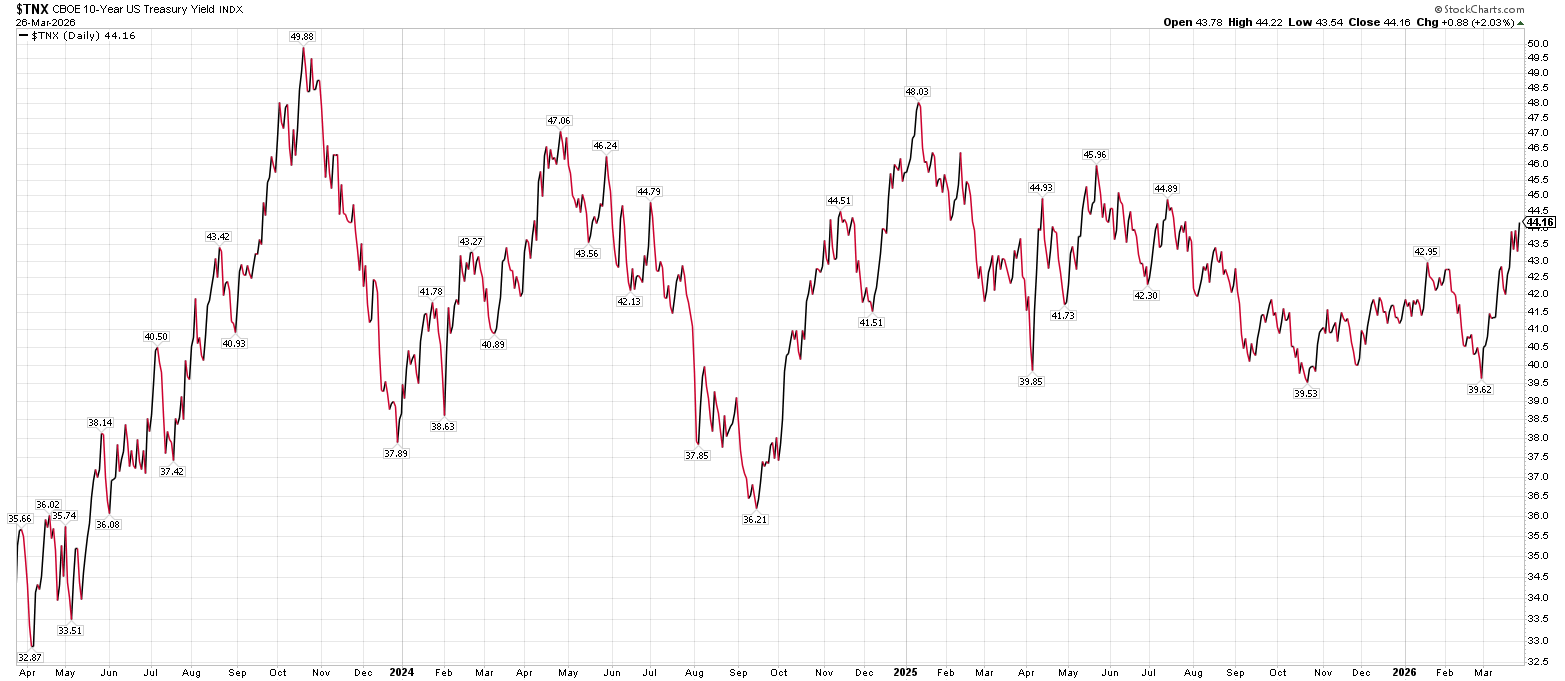

Disruptions from A.I. have caused some of the problems in private credit markets due to businesses being upended by the technology. Other issues have been caused by interest rates. While the Federal Reserve has cut rates a few times over the last 2 years, the yield on the 10-year Treasury has not given much of any relief. It currently sits around 4.4% and has seen a rapid rise this month from 3.9%. This has caused the bond market to fall right along with the stock market since the beginning of March.

The Fed continues to be in a tough spot, as recent inflation readings and the price surge in oil and gas don’t suggest inflation will be reaching their stated 2% target any time soon. We had started seeing inflation begin trending higher in the last few months even before the price surge in oil. Expectations for any more rate cuts soon doesn’t look promising. The Fed also tends to follow what rates in the Treasury market are doing, and those don’t suggest the Fed should be lowering any time soon either. Looking at the economy/employment side of things though doesn’t suggest the Fed should necessarily be increasing rates either. A surprise rate increase this year is something markets weren’t expecting and would certainly reprice things.

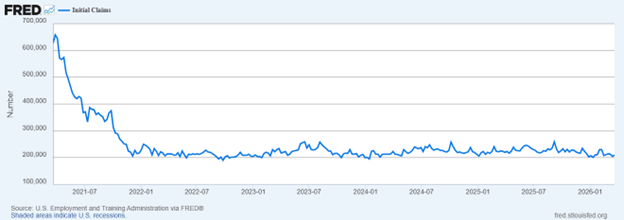

The employment picture can be best described by what some have called it a “no hire, no fire” environment. Job creation has stalled and has averaged fewer than 5,000/month since January 2025. The trend over the last 4 years of revising previous monthly job gains lower has continued. Despite this, the unemployment rate remains relatively low at 4.4% and has had just a slow increase over the last few years. Weekly jobless claims also remain historically low as you can see below. Expectations for A.I. to disrupt employment and cause large job losses throughout the economy aren’t showing up at this time.

In summary, while crises and war can cause fear and panic and may move markets in the short term, they won’t make or break the market by themselves. There are more issues domestically I believe that in combination with what’s happening in the world can create a tail risk. Watching support and resistance levels on the indexes will continue to be important, and seeing what industries and sectors lead the direction. As always, reach out with questions or concerns.

Cory McPherson is a financial planner and advisor, and President and CEO for ProActive Capital Management, Inc. He is a graduate of Kansas State University with a Bachelor of Science in Business Finance. Cory received his Retirement Income Certified Professional (RICP®) designation from The American College of Financial Services in 2017.

DISCLOSURE

ProActive Capital Management, Inc. (PCM”) is registered with the Securities and Exchange Commission. Such registration does not imply a certain level of skill or training.

The information or position herein may change from time to time without notice, and PCM has no obligation to update this material. The information herein has been provided for illustrative and informational purposes only and is not intended to serve as investment advice or as a recommendation for the purchase or sale of any security. The information herein is not specific to any individual's personal circumstances.

PCM does not provide tax or legal advice. To the extent that any material herein concerns tax or legal matters, such information is not intended to be solely relied upon nor used for the purpose of making tax and/or legal decisions without first seeking independent advice from a tax and/or legal professional.

All investments involve risk, including loss of principal invested. Past performance does not guarantee future performance. This commentary is prepared only for clients whose accounts are managed by our tactical management team at PCM. No strategy can guarantee a profit.

All investment strategies involve risk, including the risk of principal loss.

This commentary is designed to enhance our lines of communication and to provide you with timely, interesting, and thought-provoking information. You are invited and encouraged to respond with any questions or concerns you may have about your investments or just to keep us informed if your goals and objectives change.