By Cory McPherson

August 2025

In past newsletters when discussing the economy and our country’s gross domestic product (GDP), I’ve highlighted how consumer spending represents about two-thirds of what our GDP is. Basically, our economy’s main engine is run by our people’s ability to continue to spend and spend and spend. In this newsletter I’ll highlight how a new area of non-consumer spending has become more important to our GDP this year. I’ll also touch on the lofty valuations being seen due to this AI boom and how the S&P 500 continues its uninterrupted uptrend.

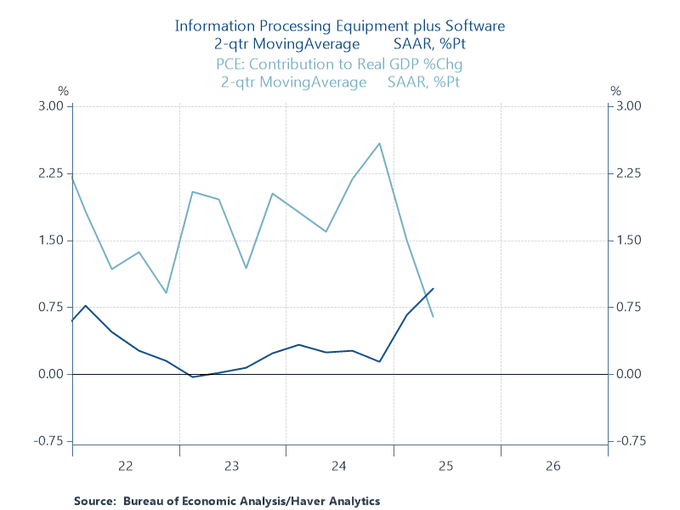

While consumer spending has continued to slow down this year, the big tech companies have spent so much on data centers in 2025 that their spending is now contributing more to economic growth than consumer spending. The main players investing at staggering levels to build and upgrade data centers are Microsoft, Google, Amazon, and Meta (Facebook). This is to support the demand for artificial intelligence (AI) computing power, with those 4 companies currently forecasting to spend $364 billion of capital investment in 2025. Analyst estimates from Renaissance Macro Research shows that so far in 2025, the value contributed to GDP growth by these capital expenditures has surpassed the impact from all U.S. consumer spending. The chart below highlights the increase in AI capital expenditure, shown as information processing equipment plus software, versus the slowdown in consumer spending.

Data from global management consulting firm, McKinsey & Company, projects that between 2025 and 2030, tech companies worldwide will need to invest $6.7 trillion into new data centers to keep up with AI demand. Spending has already been estimated to have grown 10-fold since 2022. The spending by the big tech companies has had an obvious impact on the economy. Without this spending, it’s possible the economy may have or would soon be in contraction. The money that has been flooding into AI infrastructure is also being diverted from other sectors and parts of the economy. Venture capital funding is mostly only going to AI projects now. The spending as a percentage of GDP is already larger than the peak in telecom spending during the dot-com bubble era of the late 1990’s and 2000.

So, while this has benefited the economy and kept GDP afloat, are there possible negatives to this AI spending boom? Aside from what one may think of AI in general and its eventual effects on humanity, there can certainly be unintended consequences, like that of capital being aggressively diverted from other places. This can lead to layoffs in the other sectors of the economy where access to capital dries up. There is already a fear, and a realized one for some, that AI will eventually replace a large portion of the workforce. It seems that it may very well drive job losses even before it has been widely deployed, in possibly sectors that one wouldn’t have thought would be affected. There is also the problem of the data centers and their expected ongoing cost and lifespan. The hardware is run at extremely high utilization rates and temperatures which continuously wears out the equipment. And with the pace of innovation being extremely fast, the actual hardware in the data centers quickly become obsolete. It’s estimated that the AI data center GPUs may only last 1-3 years. The next question then is, how do these data centers start creating enough revenue and become profitable with the amount of initial capital expense and expected ongoing expense? It’s unlikely these tech companies just continue to spend like this in perpetuity. They will also eventually need to have some type of return on investment. A recent report from the Massachusetts Institute of Technology found that 95% of organizations using AI are not making any money off of it despite the widespread promotion of the technology.

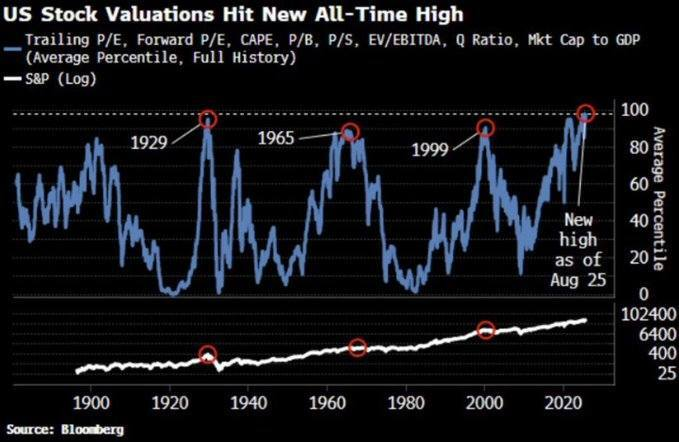

With this AI boom it has created lofty valuations for the largest tech companies in the stock market. The concentration into these companies also continues to grow. There are many ways to fundamentally value the stock market and valuations have been stretched for quite a few years now. The chart below shows a combination of different valuation metrics and their average percentile over time. Obviously where we’re at now doesn’t stand well when compared to previous periods when valuations have been this high.

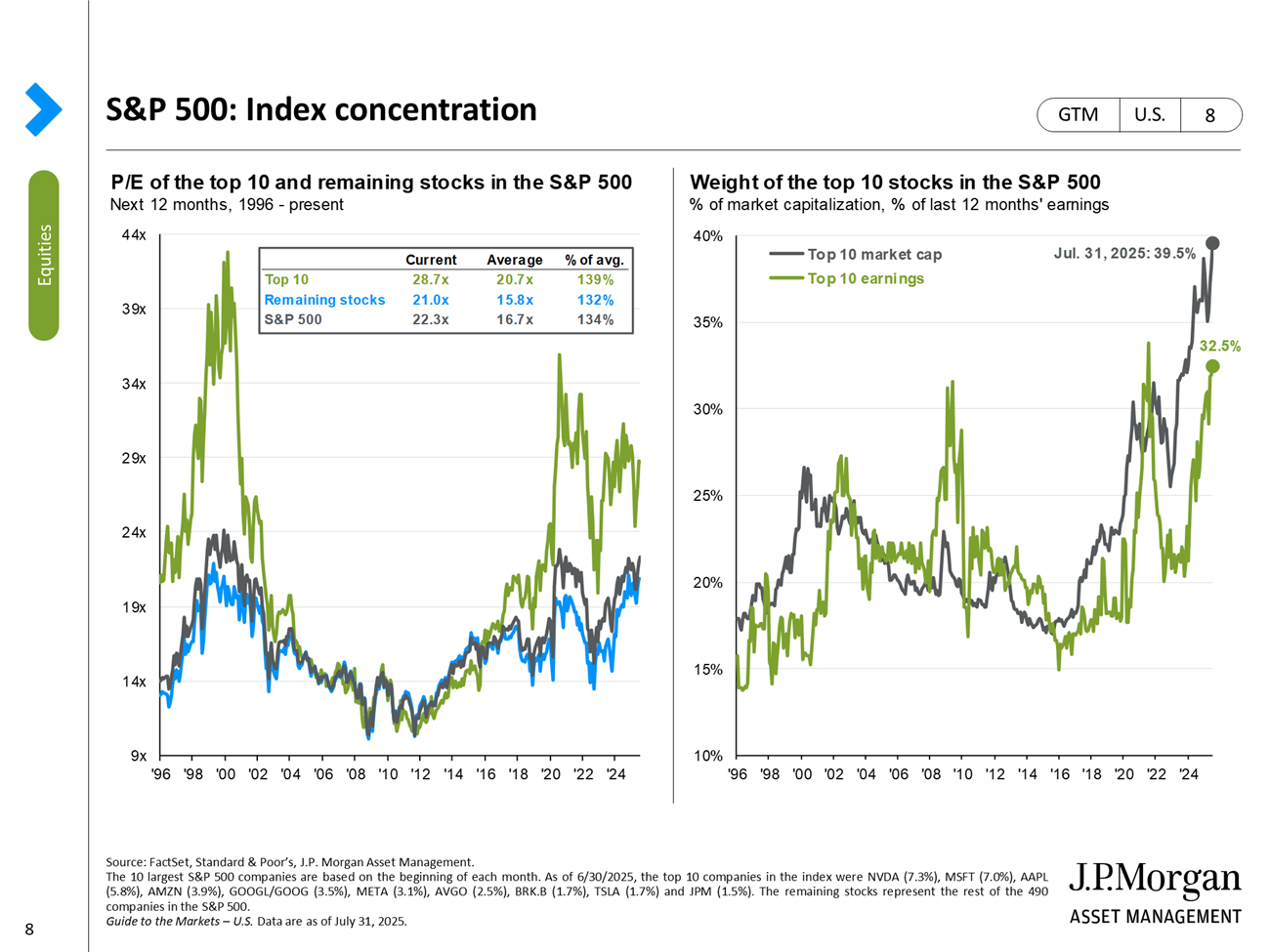

In looking at stock market concentration, the largest tech companies have had a large share of the market cap for a quite a few years. It also continues to rise and reach lofty levels. The top 7 stocks in the S&P 500 make up about 35% of the market cap. Add in the next 3 largest, the top 10 stocks of the S&P make up almost 40% of the market cap. During the peak of the dot-com bubble, the top 10 made up about 26%. The earnings of the top 10 also make up a large share of the S&P earnings. Although you can see there is a disconnect between the growth of the top 10 and their earnings trying to play catch up.

With the high concentration and nosebleed valuations, does this mean the stock market has to come down? History tells us that eventually yes it will and we will enter a lengthy bear market. It doesn’t mean that it’s happening tomorrow or next month though. The timing part of it is anyone’s guess. Valuations and concentration can get even more extreme. The more extreme it gets though, the worse the eventual outcome will be.

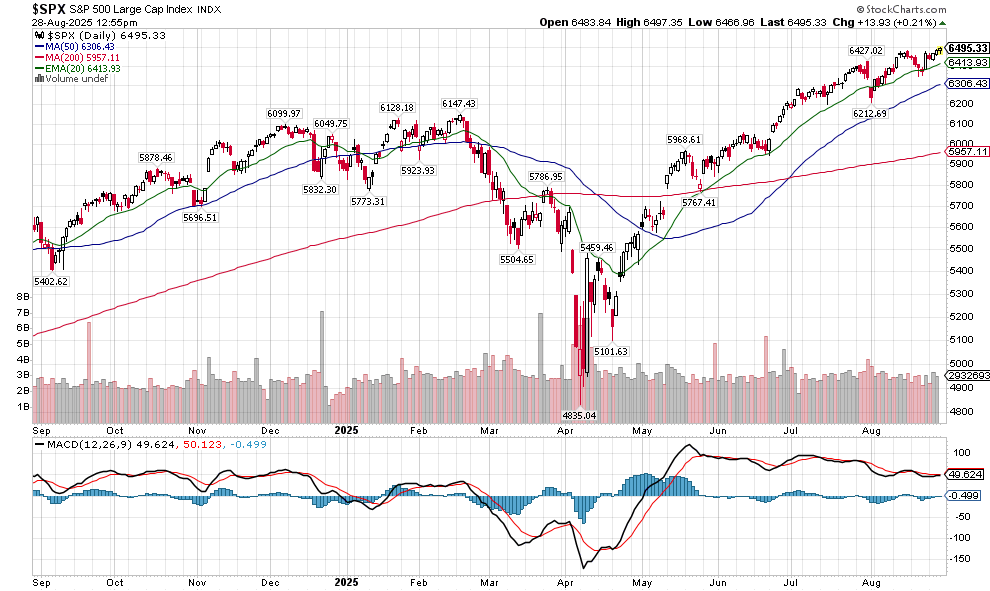

As you can see above, the S&P 500 has continued its march higher over the last month. The sudden drop at the beginning of the month and the middle of the month was quickly bought up and price recovered. It continues to trend along its 20-day moving average (green line) and has spent very little time below it since late April. You’ll notice the trend of slowing momentum has continued even as price has stretched higher this month. September has historically been a weak period for the market and while the conditions are there for a correction, until price breaks any type of support it’s hard to bet against it continuing to trend higher.

We hope everyone has enjoyed their summer and will take time to relax on this Labor Day weekend. As always, reach out with any questions or concerns.

Cory McPherson is a financial planner and advisor, and President and CEO for ProActive Capital Management, Inc. He is a graduate of Kansas State University with a Bachelor of Science in Business Finance. Cory received his Retirement Income Certified Professional (RICP®) designation from The American College of Financial Services in 2017.

DISCLOSURE

ProActive Capital Management, Inc. (PCM”) is registered with the Securities and Exchange Commission. Such registration does not imply a certain level of skill or training.

The information or position herein may change from time to time without notice, and PCM has no obligation to update this material. The information herein has been provided for illustrative and informational purposes only and is not intended to serve as investment advice or as a recommendation for the purchase or sale of any security. The information herein is not specific to any individual's personal circumstances.

PCM does not provide tax or legal advice. To the extent that any material herein concerns tax or legal matters, such information is not intended to be solely relied upon nor used for the purpose of making tax and/or legal decisions without first seeking independent advice from a tax and/or legal professional.

All investments involve risk, including loss of principal invested. Past performance does not guarantee future performance. This commentary is prepared only for clients whose accounts are managed by our tactical management team at PCM. No strategy can guarantee a profit.

All investment strategies involve risk, including the risk of principal loss.

This commentary is designed to enhance our lines of communication and to provide you with timely, interesting, and thought-provoking information. You are invited and encouraged to respond with any questions or concerns you may have about your investments or just to keep us informed if your goals and objectives change.